The Administration of Estates

Administering a deceased person’s estate can be a complicated, emotional and stressful job.

The time it will take and the level of complexity and resulting costs will depend upon the nature and size of the deceased’s estate and the terms of any Will or the impact of the rules that apply when someone dies without a Will – the Rules of Intestacy.

-

- Georgia Bolton

- Associate Solicitor

-

- Emma Cherry

- Court of Protection Assistant

-

- Robert Ashworth

- Head of Wills & Estates

-

- Ann Coutts

- Senior Associate Solicitor

-

- Carlie Brown

- Associate, Chartered Legal Executive

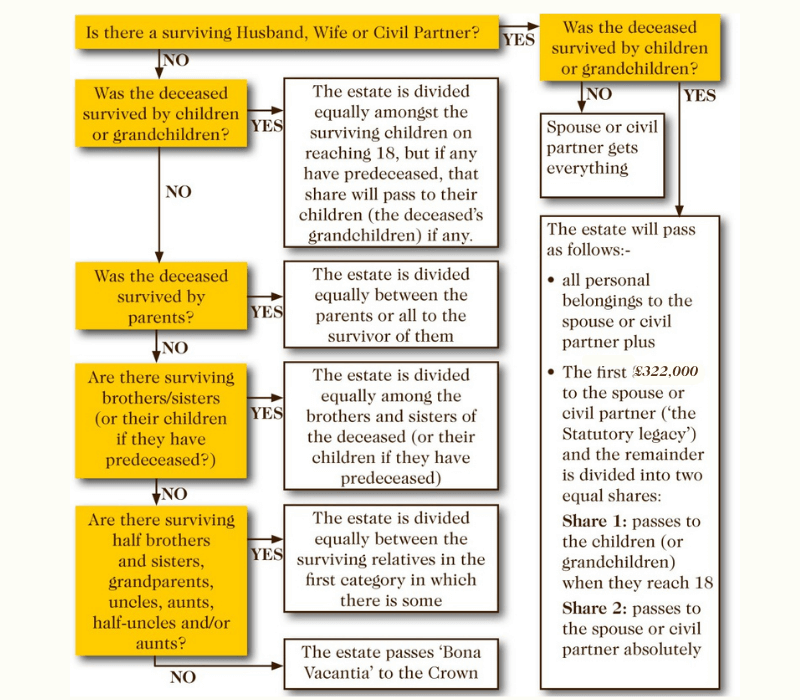

If you do not have a valid Will in place at the time of your death then the Rules of Intestacy will determine how your estate will be divided amongst your heirs. These rules can be summarised as follows:

However, the first thing you will need to think about is registering the death and arranging the funeral. TSP does not usually get involved in these arrangements unless we are acting as Executors on the estate. Funeral Expenses will need to be paid. If there is money available it is usually possible to arrange for the deceased’s bank or building society account to pay the funeral account directly.

Once this is taken care of you can think about the Estate Administration. The size and nature of the estate will determine whether it is necessary for the Executor(s) (where there is a Will) or the Administrator(s) (where there is no Will) to apply to the Probate Court for legal authority to deal with the estate, e.g. to release money held in bank accounts, sell shares, transfer or sell a house. This legal authority is called the Grant of Representation, specifically a Grant of Probate if there is a Will and a Grant of Letters of Administration if there is not.

The term probate, which. by definition, means the exhibiting and proving of a Will by the executors is in common usage as a general term to describe the process of obtaining a Grant of Representation.

Applying for a Grant of Representation is the first stage of the Estate Administration process. The second stage is gathering and distributing the assets of the deceased’s estate and carrying out the instructions in the Will or following the Rules of Intestacy.

The Wills and Estates team at Thompson Smith and Puxon can help with both stages of the estate administration or just the first or second stage. They are happy to be flexible, giving as much support to the Executors / Administrators as they need to ensure the administration is completed in an efficient and timely manner.

The key stages in an application for the Grant of Representation are detailed below:

If there is a Will – Who is named in the Will as Executor? They are the person or people entitled to administer the estate, and all the assets of the deceased pass to the executors to deal with.

If there is no Will – The person or people entitled to administer the estate, the Administrator(s), will be, in order of priority:

- Surviving spouse or civil partner

- Children of the deceased

- Parents of the deceased

- Brothers and sisters of the deceased

We will identify the legally appointed executors / administrators and advise on the type of application to the Probate Court you will require.

A comprehensive picture of the assets and liabilities of the deceased at the date of death is required. Firstly, this means collating documentary evidence such as passbooks, bank statements, share certificates, insurance policies, premium bonds, income bonds, utility bills, council tax bills, water rate bills, the funeral account, etc. Letters must be written to all asset-holders and the value of each asset obtained, including accrued interest, as at the date of death. Professional valuation may be required if the deceased owned a house or land, or a stockbroker’s help needed if there is a shareholding.

Information about any lifetime gifts made by the deceased in the last 7 years of their life should also be gathered as this will affect the available tax free allowance for Inheritance Tax (IHT).

This part of the process can be dealt with by the Executors / Administrators themselves or the TSP Wills and Estates team can take care of this for you.

Statutory Notices are placed to protect the estate against claims from unknown creditors. These notices are usually placed in the London Gazette and in the Local newspaper. TSP will, if you wish, place these notices on your behalf. We will pass the charges that we incur for placing these notices back to you. These notices remain in place for a period of 2 months before they expire.

Once the value of the assets and liabilities has been received and confirmed we will prepare a statement of the estate which we will forward to the Executors / Administrators for their approval.

A calculation of whether IHT is payable can then be made and the necessary forms filled in for reporting to HMRC. There is a handy online calculator here that can be used to give an indication of whether IHT may be payable on an estate.

Regardless of whether IHT is payable or not it may be necessary, depending on the specifics of the individual estate to complete an IHT Form 217. We will do this as part of the application grant application process.

If IHT is not payable we will need to complete an IHT Form 205. This is a much simpler and easier to complete for then the IHT Form 400 which will need to be completed if IHT is due on the estate or if the deceased has made gifts in the last 7 years of their life, even if there is no IHT to pay.

If Inheritance tax is due on the estate it must be paid, or at least the first instalment, to HMRC before the Grant of Representation can be applied for. Arrangements for payment will be discussed with the Executors / Administrators.

If you have instructed a solicitor to deal with the estate then attendance at Court is not required and the application can be submitted by the completion and Swearing of an Oath, which we will arrange, in the presence of an independent solicitor, or by submitting a Statement of Truth.

Each Executor / Administrator will need to swear the oath on each exhibit /document. The exhibit will be the Will and possibly a Codicil if there is one. There will be a charge, per executor for swearing the Oath, currently £7, and a charge per exhibit, currently £2.

If you are not using the services of a solicitor the application can be made in person to the Court, this may however require attending Court for an interview.

At the same time as the Executors / Administrators swear the Oath we will go through the application papers with them. We will then submit the application to the Probate Court and lodge the papers to obtain the Grant. There is a Court fee for this which is £155 if you are using a solicitor. There is no charge if the estate is valued at less than £5,000.

Once the Probate Court is satisfied with the application and any IHT due at that stage has been paid, the Court will retain the original Will and issue the Grant and a number of official copies. If you require additional copies of the Grant there will be a fee for this.

The Grant gives the Executors or Administrators the power to withdraw, transfer and sell the assets of the estate. Copies of the Grant plus forms of authority signed by the Executors or Administrators will be sent to the asset-holders requesting release or transfer of the assets held by them.

Following receipt of the Grant the key stages in the work needed to gather and distribute the assets according to the Will or the Rules of intestacy are as follows:

Amongst other things, the Executors or Administrators must make sure all debts have been paid and beneficiaries identified – All debts that are known of must be paid before any gifts from the estate. There may also be debts or beneficiaries that are not known of. If this is thought to be a risk then the Executors or Administrators should place statutory notices to advertise for such debts or beneficiaries. These notices remain in place for a period of 2 months before they expire.

Send the Grant of Representation and the letters of authority to the financial institutions. Collect the assets and pay any liabilities.

Amongst other things, the Executors or Administrators must deal with the deceased’s Income Tax and Capital Gains Tax (CGT). The Executors or Administrators must settle the deceased’s income tax affairs and CGT affairs to the date of death, usually by making a final tax return to HMRC; and there must be a return relating to income earned during the period of administration of the estate.

Correspond with beneficiaries regarding the distribution of the estate; pay any interim legacies

An Executor or Administrator cannot be compelled to make a distribution from the estate until at least a year has passed since the date of death, and more specifically not within six months of the grant being issued. This is because anyone who wishes to make a claim on the estate can do so during this period. However, in some circumstances the estate may be ready to be finalised before the end of the year, and the Executors make a decision about distribution at that time.

Once the estate has received money from the banks, building societies, sale of property etc., all debts should be paid and statutory notices should be allowed to expire before any legacies or payments of the residuary estate are made.

If substantial funds are held, an interim payment may be made to the beneficiaries.

We will need to check that the beneficiaries are not undischarged bankrupts – If they are then any benefit should be made to the Trustee in Bankruptcy and not to the beneficiary. There will be a charge of £2 for each bankruptcy check undertaken.

Once all assets have been collected, debts paid, tax issues settled, legacies paid and the residuary estate calculated, Estate Accounts will be prepared for the Executors or Administrators to approve. On receipt of approved Estate Accounts, the residue of the estate will be paid out to the Residuary Beneficiaries in accordance with the Will or Intestacy.

The Executors and Administrators must obtain formal clearance from HMRC that all taxes are settled and their file is closed before making final distributions.

Contact our Solicitors in Colchester or Clacton

We’re here to help. Get in touch or contact one of our offices: